The HBS Blog offers insight on Delaware corporations and LLCs as well as information about entrepreneurship, startups, cryptocurrency, venture capitalism and general business topics.

Calling and Holding a Board Meeting in a Delaware Corporation

By

Brett Melson

Monday, June 22, 2026

Learn about the rulings surrounding corporate board meetings and their relationship with the corporation’s bylaws. Read part 1 of our 2-part blog series today... Read More

Learn about the rulings surrounding corporate board meetings and their relationship with the corporation’s bylaws. Read part 1 of our 2-part blog series today... Read More

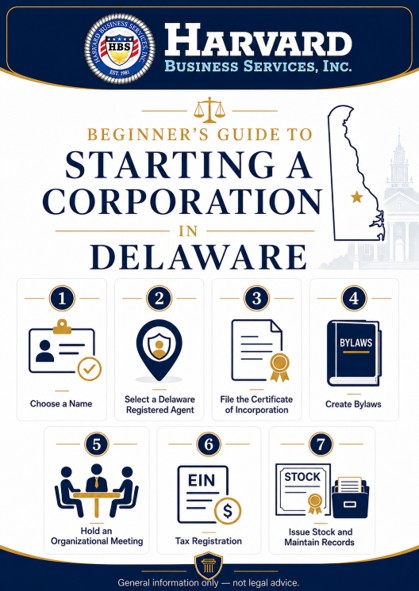

Beginner's Guide to Starting a Corporation in Delaware

By

Rick Bell

Tuesday, June 16, 2026

Anyone can form a Delaware corporation. Find out how to start a business of your own with our beginner's guide at Harvard Business Services, Inc... Read More

Anyone can form a Delaware corporation. Find out how to start a business of your own with our beginner's guide at Harvard Business Services, Inc... Read More

7 Steps to Form a Delaware LLC

By

Rick Bell

Tuesday, June 16, 2026

Find out how to form a Delaware LLC in seven easy steps. You can also work with Harvard Business Services, Inc. to form a business online... Read More

Advantages of a Delaware Close Corporation

By

Devin Scott

Tuesday, June 16, 2026

A General Corporation can have as many shareholders as it sees fit. With a Close Corporation, there are restrictions on the sale or transfer of stock. The sale or transfer of stock in a Close Corporation can be restricted by the Right of First Refusal clause... Read More

A General Corporation can have as many shareholders as it sees fit. With a Close Corporation, there are restrictions on the sale or transfer of stock. The sale or transfer of stock in a Close Corporation can be restricted by the Right of First Refusal clause... Read More

Board Meetings and the Importance of Well-Drafted Minutes

By

Brett Melson

Monday, June 15, 2026

Learn about the importance of properly recording your board meeting minutes and some of the essentials that should be included in each document... Read More

Divisive Merger Provisions under Delaware Law

By

Brett Melson

Tuesday, June 9, 2026

Under new provisions, limited liability companies and limited partnerships can develop a plan to divide the business and its assets and liabilities among two or more newly-created entities, with each business continuing independently... Read More

Under new provisions, limited liability companies and limited partnerships can develop a plan to divide the business and its assets and liabilities among two or more newly-created entities, with each business continuing independently... Read More

Ensuring an LLC Will Have Perpetual Existence

By

Brett Melson

Monday, June 8, 2026

The LLC agreement has been a popular topic in many other blog postings. This post focuses on the LLC’s potential for perpetual existence, highlighting just how flexible the Delaware LLC can be and why over 70% of our new formations are the Delaware LLC!.. Read More

Should I Obtain a Registered Agent Even When Working from Home?

By

Justin Damiani

Tuesday, June 2, 2026

Running a business from home still requires a registered agent in your state of incorporation. Learn the legal requirements, why your availability matters, privacy considerations, and options for appointing a professional agent to handle important documents while you focus on growing your home-based business... Read More

Running a business from home still requires a registered agent in your state of incorporation. Learn the legal requirements, why your availability matters, privacy considerations, and options for appointing a professional agent to handle important documents while you focus on growing your home-based business... Read More

Book Review: Warren Buffett: 43 Lessons for Business & Life

By

Devin Scott

Monday, June 1, 2026

Discover 43 life lessons followed by Warren Buffet that will help you grow as an individual and as an entrepreneur. Read our book review today... Read More

Discover 43 life lessons followed by Warren Buffet that will help you grow as an individual and as an entrepreneur. Read our book review today... Read More

Compliance is Key for your Delaware Company

By

Justin Damiani

Monday, May 25, 2026

Maintaining compliance for your Delaware company is crucial for the success of the business. Learn about what makes corporate compliance so important... Read More

Maintaining compliance for your Delaware company is crucial for the success of the business. Learn about what makes corporate compliance so important... Read More

Email this article to a friend