The HBS Blog offers insight on Delaware corporations and LLCs as well as information about entrepreneurship, startups, cryptocurrency, venture capitalism and general business topics.

Changes to Delaware’s Corporate Franchise Tax Fees

By

Amy Fountain

Wednesday, November 1, 2017

The Delaware General Assembly passed House Bill 175, which affects some taxes and fees imposed by Delaware’s Secretary of State. All the amendments have been approved. Some are already in effect and some will not be applicable until January 1, 2018... Read More

The Delaware General Assembly passed House Bill 175, which affects some taxes and fees imposed by Delaware’s Secretary of State. All the amendments have been approved. Some are already in effect and some will not be applicable until January 1, 2018... Read More

How to Operate a Delaware Company in South Carolina

By

Devin Scott

Monday, October 30, 2017

If you would like to operate a Delaware company in South Carolina, you must complete the process of Foreign Qualification in order to register your business as a foreign entity there... Read More

If you would like to operate a Delaware company in South Carolina, you must complete the process of Foreign Qualification in order to register your business as a foreign entity there... Read More

Want to Register a Delaware Company in Rhode Island?

By

Devin Scott

Monday, October 23, 2017

You can operate a Delaware company in any state, as long as you foreign qualify the company and stay in compliance in both your domestic and foreign state... Read More

You can operate a Delaware company in any state, as long as you foreign qualify the company and stay in compliance in both your domestic and foreign state... Read More

Form a Delaware Company for Your Cryptocurrency Venture

By

HBS

Monday, October 9, 2017

Bitcoin, Ethereum, Zcash, Litecoin and others—cryptocurrency may be how we spend and send money in the near future. There are tons of apps, software programs and storage sites already—do you have a cryptocurrency startup idea?.. Read More

Bitcoin, Ethereum, Zcash, Litecoin and others—cryptocurrency may be how we spend and send money in the near future. There are tons of apps, software programs and storage sites already—do you have a cryptocurrency startup idea?.. Read More

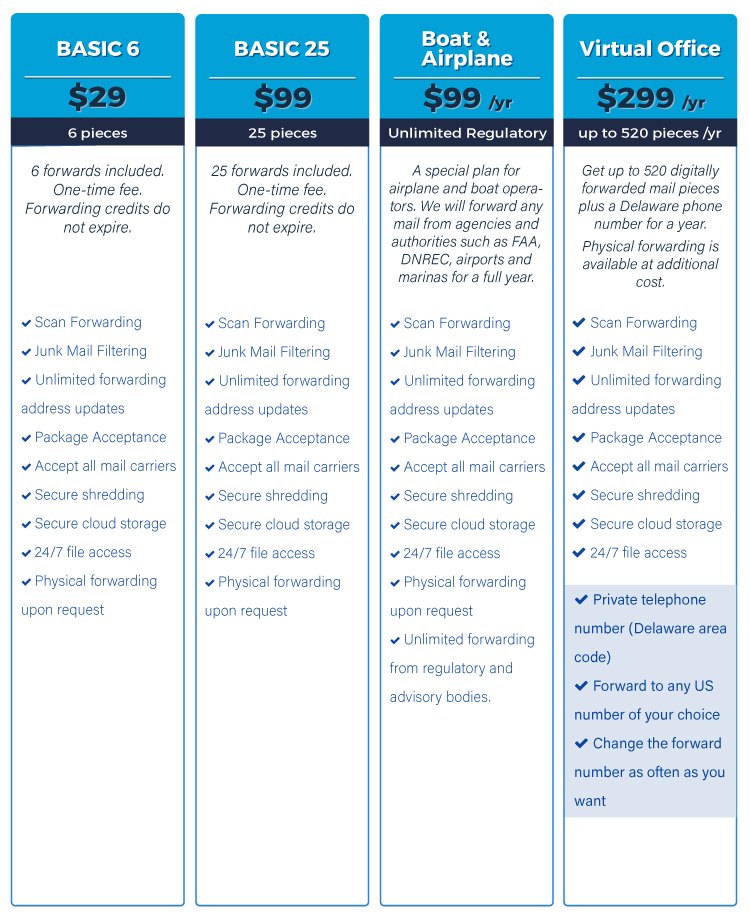

New Delaware Mail Forwarding & Virtual Office Services

By

Michael Bell

Monday, August 28, 2017

We have completely rethought and revamped our Mail Forwarding services here at Harvard Business Services. We now offer four services that are more tailored towards your business needs and the best part is we came up with new pricing... Read More

We have completely rethought and revamped our Mail Forwarding services here at Harvard Business Services. We now offer four services that are more tailored towards your business needs and the best part is we came up with new pricing... Read More

Are You Operating a Delaware Company in Indiana?

By

Devin Scott

Monday, July 31, 2017

Your Delaware company can legally operate in the state of Indiana once you file Foreign Qualification and complete the application process... Read More

Your Delaware company can legally operate in the state of Indiana once you file Foreign Qualification and complete the application process... Read More

Should You File a New Company by Yourself? [Infographic]

By

Veso Ganev

Monday, July 3, 2017

Should you file your startup company by yourself or use a business formation service? Here are the pros and cons of each... Read More

Should you file your startup company by yourself or use a business formation service? Here are the pros and cons of each... Read More

Operating a Delaware Company in Nevada

By

Devin Scott

Monday, June 26, 2017

A Delaware company doing business in the state of Nevada is considered a foreign entity and must file for Foreign Qualification, which is not difficult but is necessary to stay in compliance... Read More

A Delaware company doing business in the state of Nevada is considered a foreign entity and must file for Foreign Qualification, which is not difficult but is necessary to stay in compliance... Read More

Delaware Moves toward Blockchain Technology

By

HBS

Monday, June 19, 2017

Blockchain technology and the Delaware Blockchain Initiative are going to digitize many corporate transactions, making it easier and faster to transfer assets among companies, people, banks and law firms... Read More

Blockchain technology and the Delaware Blockchain Initiative are going to digitize many corporate transactions, making it easier and faster to transfer assets among companies, people, banks and law firms... Read More

Delaware Series LLC Operating Agreement & Structure

By

Brett Melson

Tuesday, May 16, 2017

Under Delaware law, a series LLC (limited liability company) may be composed of individual series of membership interests. This type of entity is referred to as a Delaware series LLC. Here's what you need to know about the Delaware series LLC, including the series LLC operating agreement... Read More

Under Delaware law, a series LLC (limited liability company) may be composed of individual series of membership interests. This type of entity is referred to as a Delaware series LLC. Here's what you need to know about the Delaware series LLC, including the series LLC operating agreement... Read More